Quarterly market commentary - December 2022

If you needed any reminder that investment markets are forward looking, then the last quarter of 2022 provided the perfect example.

Entering the final three months of the year, investors were surveying an environment that included a seemingly unending supply of negative news headlines:

- "The highest inflation in four decades"

- "Double-digit losses in both share markets and bond markets"

- "Interest rates rising rapidly"

- "Ongoing war in Ukraine"

- "Continued lockdowns in the world’s second largest economy (China)"

- "Elevated petrol prices"

- "A slowdown in the housing market"

So, what did share markets do?

They went up. In many cases, they went up strongly.

All of the 23 developed markets in the MSCI World Index were positive over the quarter and 19 went up by at least 6% (in local currency terms). It was a similar story in emerging markets where 14 of the 24 nations in the MSCI Emerging Markets Index went up by more than 6%. The gains in emerging markets were not uniform, with six emerging nations dipping into the red for the quarter.

As indicated by these results, it was a very strong quarter for share markets. The obvious question is, why? What do the markets know that we don’t?

Markets don’t actually 'know' any more than we do. The aggregate market is made up of individuals, trusts, companies, professional investors and a wide range of institutional investors. While individual investors can sometimes react poorly to the constant media ‘noise’, and occasionally make knee-jerk decisions to sell, investors that are committed to seeking longer term investment outcomes are often better able to block out this noise and focus on the value of the underlying assets.

When markets become difficult, investors that are easily influenced by emotion, uncertainty or fear are prone to making bad decisions. But for every panicked seller, we need to remember there is always a buyer (often more considered) taking an equal and opposite view.

During 2022, the prices of many good quality investments had reduced to the point that, in aggregate, market participants began to regard them as being relatively cheap. And for most long term investors, ‘quality’ plus ‘cheap’ equals an attractive investment opportunity.

Sure, there were (and are) many uncertainties in the world and the list above covers most of the big ones. But investors looking to own high quality assets for the long term, don’t need to be quite so concerned about exactly when interest rates might stop rising, when housing prices will stabilise, or even when the war in Ukraine will end.

At some point (hopefully sooner rather than later), most investors believe that all of these things will happen. And, when viewed through that lens, it’s easier to understand how the asset prices available at the beginning of the September could generally be considered attractive, regardless of what was still going on in the world around us.

Fighting inflation

The cost of living crisis was one of the big talking points of 2022 with prices, particularly at the supermarket and at the petrol pump, rising uncomfortably quickly at times.

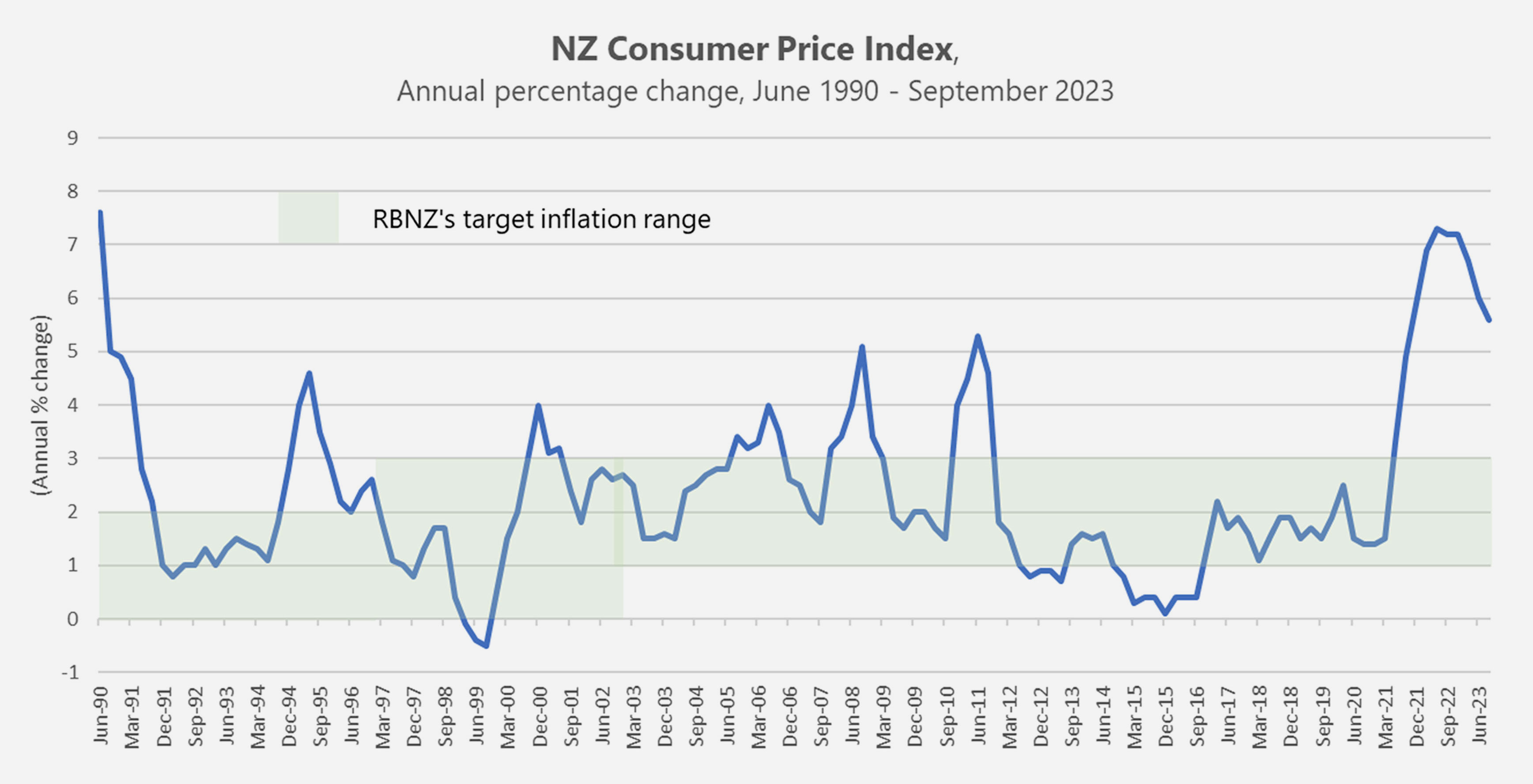

Having successfully controlled inflation within their target range of 1-3% over most of the last decade (as the following chart shows), the Reserve Bank of New Zealand (RBNZ) had also very effectively managed our collective inflation expectations. That is, we all generally expected average inflation of around 2% (give or take) to persist into the future, and our spending and investment behaviours reflected those expectations.

However, following the post-Covid surge in inflation from 2021 to the current level of 7.2% pa (as at 30 September 2022), the RBNZ has become increasingly concerned about the risk of a potential ‘de-anchoring’ of our collective inflation expectations. In other words, they are concerned we may begin to expect much higher levels of inflation into the future than we had previously.

If we begin to expect higher inflation, this is likely to impact our decision making in relation to savings, investment and spending. It is also likely to impact other areas such as wage negotiations, putting pressure on wages to continue to rise higher and higher to meet rising costs. This, in turn, flames the inflationary pressures we are already facing. If our inflation expectations were to be reset at higher levels, it presents a much bigger challenge for the RBNZ to quickly get price inflation back down towards the levels we had previously been experiencing.

Galvanised by these concerns, the RBNZ hiked New Zealand’s official cash rate (OCR) by another 0.75% at their November meeting to 4.25%, and revised their projection for the OCR to now reach a peak of 5.50% in 2023. This revised peak is a full 1.40% above the OCR forecast of 4.10% from their August announcement.

How successful the RBNZ are at curbing inflation will be something to watch this year.

The chart shows that when inflation has historically reached a short term peak of 4% or more, it has subsequently fallen reasonably quickly (usually after the RBNZ has moved interest rates higher).

If something similar can be achieved within the next one or two inflation updates, there is still a chance the projected OCR peak of 5.50% may not be required.

For now we watch and wait for more inflation data.

It should also be noted that with much of the global economy experiencing similar inflationary issues, the coordinated interest rate rising that is occurring around the world will act as a headwind to global growth in 2023. If that headwind blows too hard for too long, it increases the chances that we will see a period of lower or negative growth in some countries/regions later this year. Clearly, a delicate balancing act for central banks around the globe.

Energy sector outperforms

While it wasn’t a good year overall for share markets, there was one standout performer – the energy sector.

Higher oil and gas prices were a feature of the year, and it was one of several factors that contributed to rocketing global inflation. Although higher oil prices are generally bad news for consumers and travellers, it was great news for the energy industry (and its investors). As oil prices soared, so too did the performance of many listed energy companies.

In the US, the energy sector returned more than 65% in 2022 - its best year on record - and in Europe it was also easily the leading sector, up more than 37%. These returns are even more remarkable in a year when global share markets were broadly negative.

This represented a dramatic turnaround from the depths of 2020, when the energy sector was initially the largest casualty of the global shutdown that followed the arrival of the Covid-19 pandemic.

A much better outlook for bonds

The combination of rising interest rates and higher inflation in 2022 led not only to a bear market in shares, but the worst year for bonds in modern financial history.

As interest rates rose faster and further than all early predictions, bond prices declined by significantly more than we are accustomed to. As the year wore on, it led to some investors considering potential alternative assets, particularly ones that could also help to offset traditional share market risk.

However, just as investors may be starting to lose faith in the role that bonds play within diversified portfolios, the forward-looking prospects for bonds are now better than they have been in years.

As at 30 December, the S&P/NZX A-Grade Corporate Bond Index in New Zealand had a running yield of 5.4%, while the Global Aggregate Bond Index was yielding 4.9% in New Zealand dollar hedged terms (having touched over 5% in recent months).

With central banks now well into their interest rate tightening cycles, early signs of global inflation beginning to moderate and consumer demand seemingly softening, we have an environment for stronger bond returns than we have seen in recent years.

Also noteworthy, is that bond yields are now at levels where they have room to rally (i.e. room for bond prices to rise) if, for example, a non-inflationary macroeconomic shock were to occur and policymakers were to respond by lowering interest rates.

This more positive outlook may be tempered a little by the fact that the large government deficits that built up during the early and mid-stages of the Covid pandemic, are likely to remain elevated for some time. Even if governments are successful in taking a more frugal approach to future spending, they will need to continue selling more bonds to the private sector, and that will be happening in a financial system with reduced overall liquidity. This could limit the scope for bond yields to decline much as headline inflation falls back from peak levels.

However, even in a scenario where bond yields may remain more consistently at or around their current levels, the running yields alone, as outlined above, make them an attractive component of diversified portfolios.

All eyes on 2023

The final quarter of 2022 provided a very positive end to an otherwise challenging year for investors.

It was encouraging that in spite of the lack of clarity on a number of high profile macroeconomic, and geopolitical issues, the markets were able to look through these matters and conclude that many asset prices were increasingly looking attractive.

One strong quarter in no way guarantees that the recent challenging market conditions are fully behind us, but it is a positive sign, and it takes us into the new year with more reason for optimism about the potential for better times ahead.

If the uneven transition from Covid lockdowns to a global economic reopening has shown us anything, it’s that governments, central banks and investment markets don’t have a proven playbook about how to seamlessly return the world back to its pre-Covid state. As a result, the last few years have thrown up economic outcomes and market eccentricities that have been well outside our normal expectations.

With the potential for inflation pressures to ease in 2023 and for interest rates to stabilise, it is not unreasonable to hope that some of these eccentricities also begin to moderate.

In the meantime, when markets are as difficult to navigate as they have been lately, the very best approach is always to stay invested, stay well diversified, keep costs low, and stay patient.

For a detailed review of the asset class performances for the quarter, see ‘Key market movements - December 2022’ or click here to view the full newsletter in PDF.

Disclaimer

Information contained in this newsletter does not constitute personalised financial advice and does not take into account your individual circumstances or objectives. You should carefully consider whether the Synergy investment portfolios are appropriate for you, read the applicable offer documentation, and seek appropriate professional advice before making any investment decision. The information in this newsletter is of a general nature only. Investors should be aware that the future performance of the Synergy investment portfolios may differ from historical performance. Details are correct as at the date of preparation and are subject to change. The investment objectives and strategies of the Synergy investment portfolios may change in the future.

While every care has been taken in its preparation, Consilium makes no representation or warranty as to the accuracy or completeness of the information in this newsletter and does not accept any liability for reliance on it. The capital value, performance, principal and returns of the Synergy investment portfolios are not guaranteed or secured in any way by Consilium, or any other person. Investments in the Synergy investment portfolios do not represent deposits or other liabilities of Consilium and are subject to investment risk, including possible loss of income and principal invested.

-

Key market movements - December 2022

After such a challenging first three quarters of 2022, it was difficult to imagine the final quarter would deliver anything substantially different. As they say however, it is always darkest before the dawn.

-

12 ways to finally achieve your most elusive goals

It’s that time of year to muse on what you hope to accomplish over the next 12 months. The best advice when making resolutions is to set goals that are “SMART” – specific, measurable, achievable, relevant (to you) and time-bound. Once you’ve set your goals, what can help you achieve them? Based on our research, we’ve distilled 12 goal-enablers. These cover four broad principles you can use to keep yourself on track.

-

Quarterly market commentary - September 2022

The global economy has been buffeted by multiple challenges in 2022 and it is fast shaping as a year not many will remember fondly. During the drawn-out lockdowns and upheaval that accompanied the peaks of Covid-19, the world collectively pined for a seamless post-Covid recovery. The reality, however, has been rather bumpy.