Quarterly market commentary - December 2023

It was most appropriate that the fourth quarter of 2023 included Christmas, as it was indeed a quarter of many happy returns.

Global share markets delivered strong gains as market expectations about the future trajectory of interest rates changed markedly over the quarter. While the consensus view in the September quarter was for interest rates to remain ‘higher for longer’, the focus over the last three months was on the potential for the US Federal Reserve to successfully engineer a ‘soft-landing’ for the US economy (i.e. inflation coming back under control without unduly impacting the wider economy). Increased hopes for this goldilocks scenario, which is vastly more preferable than the economy slumping into recession, saw share prices surge.

Global bonds also joined the party. The idea that US interest rates could begin falling in 2024 led to a reduction in long term bond yields, which sent bond prices up sharply. For investors who had endured a difficult period in bond markets over the last two years, this represented a welcome holiday gift.

A noteworthy aspect in all of this is that, for the most part, not much had really changed. Yes, oil and gas prices did decline (which was a positive), but global interest rate policy settings were largely unchanged, conflict in the Ukraine and Middle East continued, and businesses generally did not report dramatically improved profits or projections. The main ingredient that changed was investor expectations.

In September, when markets were anticipating interest rates being higher for longer, this impacted a number of important calculations, notably what the current price of bonds or shares should be. However, in a scenario where interest rates were now anticipated to be lower than previously expected, investors simultaneously reassessed asset valuations. What they had considered to be 'fair' prices in September were, within a matter of only a few weeks, considered to be 'cheap'. And, like any rational consumer wanting to buy if they think they’re getting a bargain, investors did just that, pushing the prices of shares and bonds higher over the last three months of 2023.

Inflation

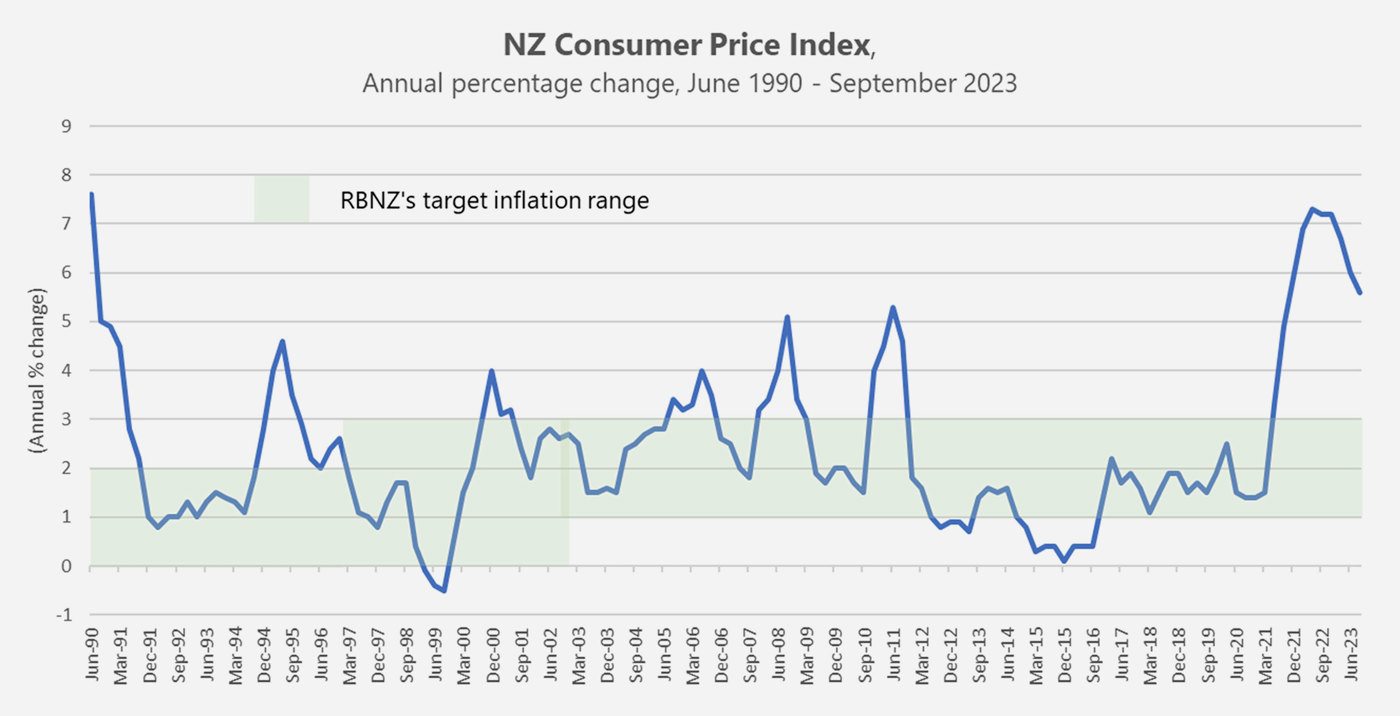

While investors have a natural interest in asset prices, central bankers are more focused on the prices of goods and services throughout the economy. Increases in the prices of goods and services is known as inflation, and central banks are tasked with, keeping that within targeted levels. In New Zealand’s case the Reserve Bank of New Zealand (RBNZ) aims to keep inflation (measured by the Consumer Price Index) between 1% and 3% over the medium term.

As the chart below shows, up until the emergence of Covid-19, the RBNZ had generally been quite successful in achieving this.

Unfortunately, the significant support payments made to businesses and workers to keep them solvent while Covid lockdowns were in place, eventually led to a spike in inflation in 2021/22. Once we all got out of lockdown, the world’s factories (and broken supply chains) needed many more months to get operating again, and it quickly became clear that global production couldn’t match the surging demand from cashed-up consumers. For a period of time, we literally had a situation where far too much money was chasing too few goods – classic inflationary conditions.

This phenomenon was experienced all over the world, but in New Zealand’s case we have been slower to see inflation come back down again. The last official reading (for the 12 months ended September 2023) had domestic inflation at 5.6% - moving in the right direction from the high of 7.3% in mid 2022, but still well outside the RBNZ’s 1% - 3% target band.

While the talk in the December quarter turned to the likelihood of US interest rates beginning to come down in 2024, the jury is still out about what will happen to New Zealand interest rates. Inflation in the US is only 3.1%, while ours is nearly double that, and the RBNZ will be reluctant to risk cutting interest rates too early for fear of reigniting another round of inflationary pressure here.

Migration

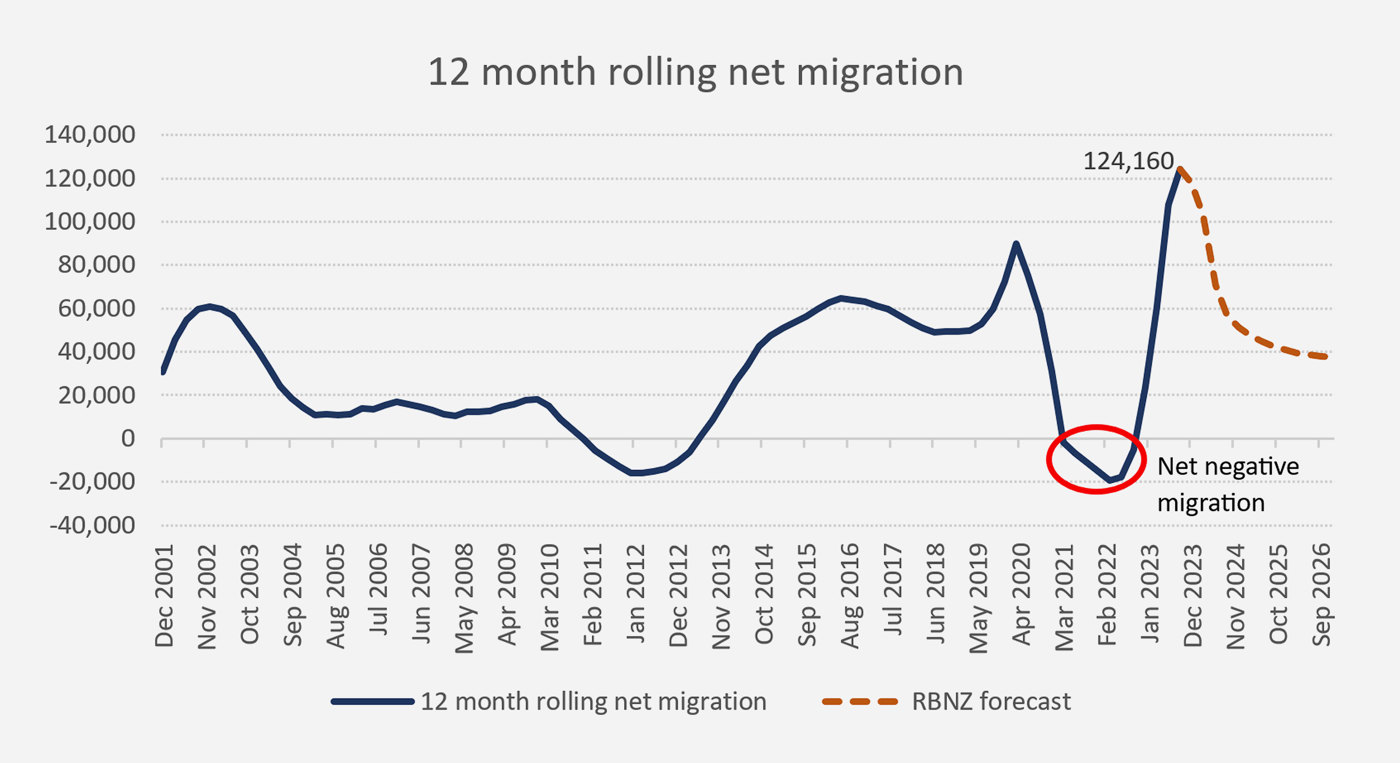

For the roughly two years when New Zealand’s borders were closed, we experienced net negative migration. However, once borders were eventually re-opened, net migration skyrocketed. In the 12 months to September 2023, we have welcomed over 124,000 more people to New Zealand to live, over and above the number that have chosen to leave. As the chart below shows, that represents easily the largest annual increase in net migration this century.

As everyone that comes to New Zealand needs somewhere to live and will generally either buy or rent some accommodation, it's no wonder that unexpectedly high migration is now a significant factor in the RBNZ’s sensitivity to high inflation. After all, housing costs make up almost 30% of the Consumer Price Index and almost half of New Zealand’s non-tradable inflation.

From this current peak, the RBNZ are forecasting net migration to slow down quite quickly to a level of around 40,000 per annum by 2026. However, if this doesn’t happen – if net migration stays higher for longer – then this is likely to put further pressure on rents and house prices and, unfortunately, inflation.

In that event, for the RBNZ to continue to make progress towards meeting its medium term inflation target, they will either need to see greater disinflationary forces coming from other parts of the economy and/or consider a tighter monetary policy stance than they might otherwise prefer (i.e. higher interest rates).

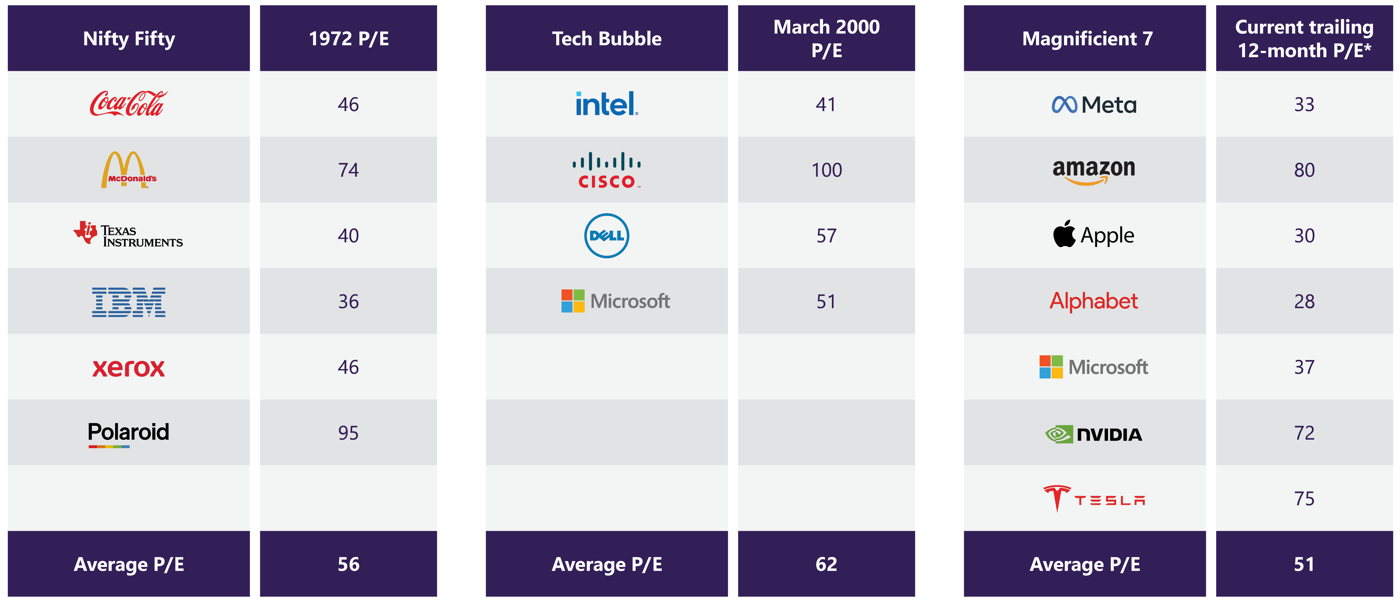

The Magnificent 7

While the main US share index (the S&P 500 Total Return Index) was up 26.3% in 2023, it was the so called Magnificent 7 (comprising Meta, Amazon, Apple, Alphabet, Microsoft, Nvidia and Tesla) that was responsible for the majority of the returns.

The price performance of these companies has, without doubt, been heavily influenced by investors' growing fascination with the Artificial Intelligence (AI) story. However, history provides cautionary warnings about sky-high valuations driven by appealing stories.

As the table below demonstrates, with an average price-to-earnings (P/E) ratio of around 51, the valuations of the Magnificent 7 are fast approaching the lofty levels briefly attained by the major Nifty Fifty stocks of the 1960s and 1970s and dotcom companies in the late 1990s, just prior to them eventually crashing. What these earlier periods were both remembered for was the tendency for many investors to ignore fundamental company valuation metrics, and instead make investment decisions based on popular sentiment.

* from Yahoo finance, as at 10 January 2024

While none of the above is intended to forecast a pending crash, it is a cautionary reminder that the Magnificent 7 shares, which currently make up about 30% of the total market capitalisation of the S&P 500 index, are at historically high valuations.

For investors drawn to the AI hype, this should be considered very carefully before investing. But for most prudent, long term investors, those who are not over-allocating to just a handful of high-priced companies, the news is much better – the rest of the market has valuations that are much closer to, or below, their historical averages.

This is where having access to professional investment advice can be extremely valuable. Individual investors often struggle with something called ‘recency bias’. This leads to favouring assets that have performed well recently (for example Magnificent 7 companies) ahead of those that may have performed relatively poorly. However, professional advice usually acknowledges that chasing high priced shares can often result in overpaying and achieving an unattractive long term return as a result

A new year

In some ways, 2023 was a frustrating year. The ongoing media noise about ram raids, law and order, the cost of living crisis, doctor shortages, housing market weakness, migration issues, the election, and the conflicts in the Middle East and Ukraine, drowned out just about everything else.

One of the things it certainly drowned out was that investment markets delivered some pretty nice returns. Australian, emerging market and international developed share markets delivered double-digit returns, and the bond markets that had been decidedly weak over the last two years bounced back with strong contributions.

Of course, it wasn’t without a fair amount of volatility and uncertainty along the way, but when it comes to long term investing in risky assets, it rarely is.

If 2024 could be a repeat of 2023 in the markets, but with a happier news flow, it will be a year to look forward to!

As we enter the new year, portfolios continue to be well diversified and, as always, are well positioned to pick up returns wherever they may arise.

In the meantime, when markets are unpredictable (as they are) and forecasting the future is impossible (as it is), the best approach remains the one that strategic investors have been successfully applying for years.

That is, staying invested, staying well diversified, keeping costs low and staying patient.

For a detailed review of the asset class performances for the quarter, see ‘Key market movements - December 2023’

Click here to view the full newsletter in PDF

Disclaimer

While every care has been taken in the preparation of this newsletter, Consilium makes no representation or warranty as to the accuracy or completeness of the information contained in it and does not accept any liability for reliance on it. Information contained in this newsletter does not constitute personalised financial advice and does not take into account your individual circumstances or objectives.

-

Key market movements - December 2023

International share markets rebounded with a strong rally over the final three months of the year. While sharply lower prices for natural gas, crude oil, and gas oil contributed to lower inflationary pressures over the quarter.

-

Push for more, but be content with enough

Finding the balance between wanting more from your money, but being content with enough is an important aspect of financial wellbeing. At a basic level, the reason that any of us work to earn money is so that we can pay for things. Our wealth enables us to provide for ourselves, our families, and to sustain a certain lifestyle. But how do we strike a balance between wanting more and finding contentment?

-

Quarterly market commentary - September 2023

In some welcome news, the world economy is showing signs of resilience this year despite lingering inflation and a sluggish recovery in China. The International Monetary Fund (IMF) released its latest World Economic Outlook in July, where they noted this resilience is increasing the odds that a global recession may be avoided.