Quarterly market commentary - March 2023

Following an upbeat end to 2022, investment markets continued to deliver generally positive returns over the first three months of 2023.

In an environment where energy costs were falling globally and the large Chinese economy began to reopen (after their abandonment of strict Covid-19 controls in late 2022), sentiment about the outlook for global growth was very positive.

After months of co-ordinated central bank action to increase interest rates, headline inflation also looked to be slowly improving globally, raising expectations that the global interest rate hiking cycle could soon be coming to an end.

Unfortunately, measurements of ‘core’ inflation (i.e. the general cost of goods and services that excludes more volatile food and energy prices) stubbornly stayed higher than expected in both the US and Europe, indicating the interest rate tightening cycle still had further to run.

In early March, the collapse of Silicon Valley Bank in the US, followed a week later by troubled lender Credit Suisse being bought by global investment bank UBS, created significant, but short-lived, market turbulence.

Markets initially reacted to fears of a potential new banking crisis and bond markets quickly went from pricing in further interest rate hikes to pricing in sizable rate cuts in some markets.

However, by the end of the quarter, investors had largely concluded the events surrounding Silicon Valley Bank and Credit Suisse were contained and that any potential systemic risks were minimal.

China’s recovery accelerating

Less than six months ago, the Chinese economy was partly locked down with Covid restrictions and its economic performance was dwindling as a result.

Fast forward to today, and indicators are currently pointing to a solid recovery in Chinese economic activity. This renewed strength is directly contributing to an improved sentiment for global growth.

Notably, the current recovery in China is stronger than when they initially reopened earlier in the pandemic. This suggests a greater degree of confidence in the recovery this time around.

While this is good news for China it also bodes well for other economies, particularly those with a large trading relationship with China. Europe and Asia are well placed to benefit, and the Australian economy stands to be a direct beneficiary of improving volume and pricing for mineral exports, particularly iron ore and copper.

Global growth to rebound in 2024

In January, the International Monetary Fund (IMF) announced that while the global economy is poised to slow from a growth rate of 3.4% in 2022 to 2.9% this year, they are now projecting growth to rebound to 3.1% in 2024.

Although they noted the war in Ukraine and the global fight against inflation remained risks, the IMF nevertheless reported a mild upward revision to their October 2022 projections. In particular, they commented that the global economy had shown great resilience over the recent period and that a global recession is not their baseline view.

We are well acquainted with the difficulties in accurately forecasting the future, however this is still encouraging. At a minimum, it tells us that the wide-ranging economic data the IMF are basing their forecasts on are showing some overall improvement.

While it’s possible that China's recovery could yet stall, inflation could persist at high levels and an escalation of the war in Ukraine could all contribute to a deterioration in financial conditions, the IMF also noted there were factors that could also lead to better-than-expected outcomes.

In particular, strong household balance sheets and robust wage growth could help sustain consumer demand. Additionally, an easing of the remaining supply bottlenecks, coupled with an easing in labour market pressures, could allow for a softer economic landing which would require less monetary tightening than is currently anticipated.

What is a soft landing?

The term “soft landing” refers to an objective of a central bank to slow down an economy and bring down inflation, while preventing the economy from falling into a recession. Recessions are generally defined as two consecutive quarters of negative growth, and are normally unwelcome as economic output, employment and consumer spending all come under increased pressure for a period of time.

To this end, the Reserve Bank of New Zealand (RBNZ), along with many other central banks, have implemented a series of interest rate hikes over the last eighteen months. The aim has been to try and rein in demand to slow down the rate of general price increases. For many homeowners with mortgages, increasing interest costs on their home loan will generally lead to a reduction in spending in other areas, which will usually help reduce inflation overall.

Unfortunately, the approach is not without risk. In theory, raising interest rates eventually cools demand and brings down prices, but the mechanism is often described as a ‘blunt tool’ with an uncertain impact. It can also take months for any subsequent change in consumer spending behaviour to be confirmed. This increases the chances that policymakers inadvertently overshoot and raise interest rates by more than they needed to.

Clearly, it’s a very difficult balancing act.

Holding interest rates too low for too long helped create the current inflation problem. But if interest rates now rise too far, it increases the chance of a steeper economic downturn that more significantly impacts businesses and results in a larger spike in unemployment. That would broadly be described as a ‘hard landing’; the very outcome the RBNZ is striving to avoid.

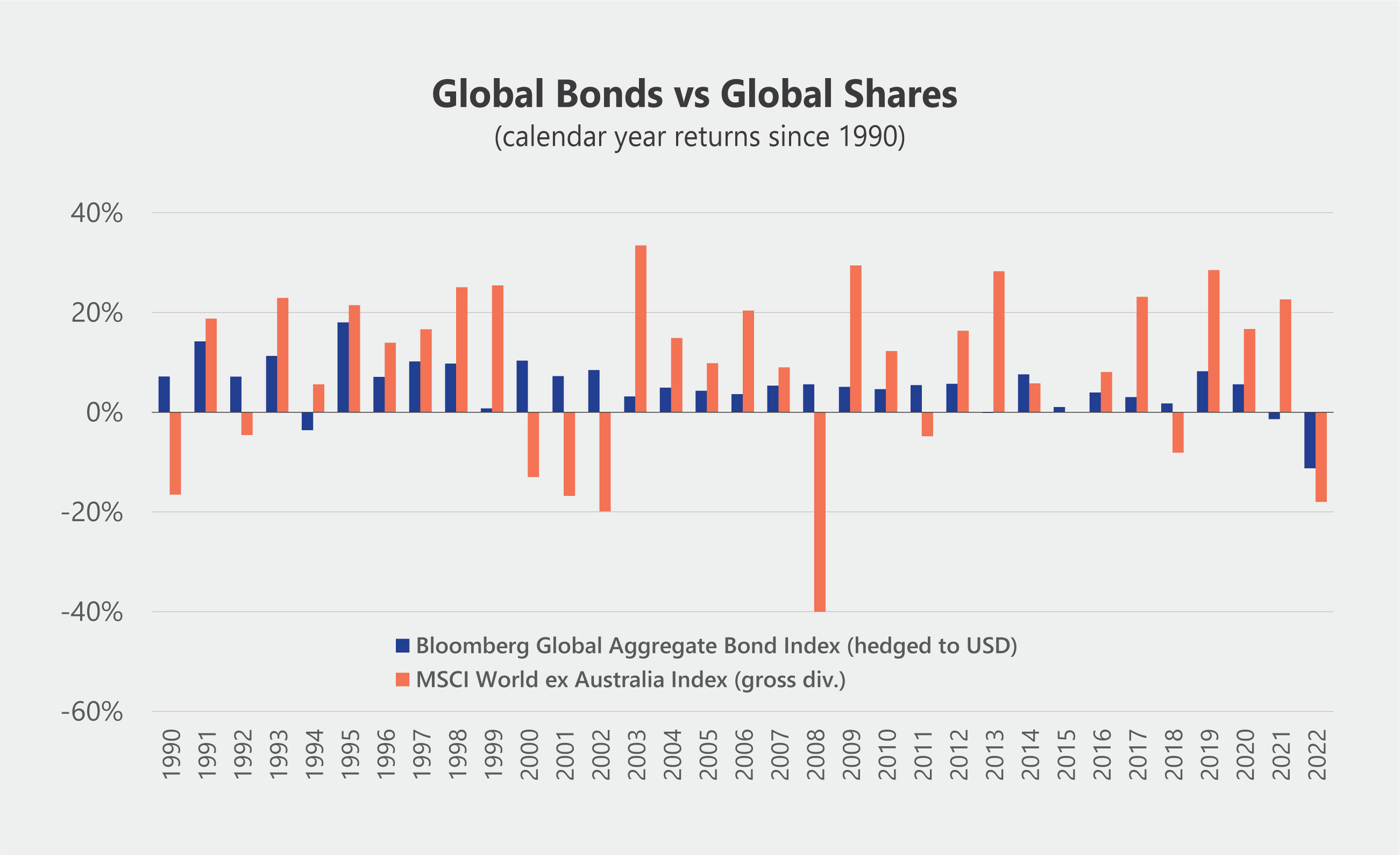

Bonds – back to the future?

As we’ve attempted to explain in various communications, the painful outcome for investors in bonds in 2022 was highly unusual. This chart helps to provide some context.

The bars on the chart show the calendar year returns from global bonds(1) (blue bars) and global shares(2) (orange bars). The performances we are showing here are in US dollars, as that gives us a longer index data set than if we were showing the same information in New Zealand dollars. However, the picture would otherwise look very similar.

The main observations we can see at a glance (or within a few glances) are as follows:

- Bond returns are usually positive. Including 2013, when bonds were down by just -0.1%, there have only been four years out of 33 when bonds have been negative.

- In contrast, global share market returns are negative more often (nine years out of 33). This is consistent with shares generally being a higher risk investment. Similarly, we also see share returns delivering much larger positive and negative returns over time.

- What’s also very interesting is when we look at the nine years when shares delivered negative returns – 1990, 1992, 2000, 2001, 2002, 2008, 2011, 2018 and 2022. In all of these years except 2022, the corresponding return from bonds was positive.

Stay focused on what works

We can’t predict the future, but we can continue to learn from the past.

As investment practitioners, we have helped clients successfully navigate some extremely difficult markets over the years.

Each periodic “crisis” has been different, and each has been as unpredictable as the last, but the best solutions have almost always looked the same:

- Stay in touch with your adviser and stick with your plan.

- By all means change that plan when your circumstances change, but not in reaction to a sudden market event.

- Be focused on the things you can control.

- Keep investment costs as low as possible and stay as diversified as you can in relation to your risk profile.

- Tune out the media noise and any investment opportunities (or salespeople) that promise to consistently beat the market – the weight of evidence is not on their side.

We know markets will continue to go up and down; they always have. Importantly, most seasoned investors also understand that we can’t pursue the potential rewards of achieving higher investment returns without accepting some risk of periodic underperformance along the way.

When it comes down to long term investment planning, the good news is that the volatility we expect from markets over time (the mixture of good and bad returns) is already factored into our projections and your plan. As a result, when returns do occasionally disappoint, your adviser will rightly remind you - unless your circumstances have otherwise changed - to stick to the plan, because that is where any short term pain ultimately gets replaced with long term gain.

(1) Using the returns of the Bloomberg Global Aggregate Bond Index (hedged to USD)

(2) Using the returns of the MSCI World ex Australia Index (gross div), in USD

For a detailed review of the asset class performances for the quarter, see ‘Key market movements -March 2023’ or click here to view the full newsletter in PDF.

Disclaimer

Information contained in this newsletter does not constitute personalised financial advice and does not take into account your individual circumstances or objectives. You should carefully consider whether the Synergy investment portfolios are appropriate for you, read the applicable offer documentation, and seek appropriate professional advice before making any investment decision. The information in this newsletter is of a general nature only. Investors should be aware that the future performance of the Synergy investment portfolios may differ from historical performance. Details are correct as at the date of preparation and are subject to change. The investment objectives and strategies of the Synergy investment portfolios may change in the future.

While every care has been taken in its preparation, Consilium makes no representation or warranty as to the accuracy or completeness of the information in this newsletter and does not accept any liability for reliance on it. The capital value, performance, principal and returns of the Synergy investment portfolios are not guaranteed or secured in any way by Consilium, or any other person. Investments in the Synergy investment portfolios do not represent deposits or other liabilities of Consilium and are subject to investment risk, including possible loss of income and principal invested.

-

Key market movements - March 2023

Global share markets delivered further positive results in the first quarter, buoyed by a reduction in recession concerns across leading developed markets.

-

23 ways the world is getting better

This is the greatest time in history to be alive. The world has seen an unbelievable amount of progress over almost any time horizon you look at.

-

Quarterly market commentary - December 2022

If you needed any reminder that investment markets are forward looking, then the last quarter of 2022 provided the perfect example. Entering the final three months of the year, investors were surveying an environment that included a seemingly unending supply of negative news headlines... So, what did share markets do? They went up. In many cases, they went up strongly.